mortgage distress – Misryoum reports where mortgage stress is rising and why early delinquencies matter for potential foreclosure risk.

A growing wave of early missed payments is offering a glimpse into where mortgage stress may be heading next.

In the U.S., the timeline is familiar: borrowers typically begin with 30- or 60-day delinquency before falling further behind.. If financial pressure persists. loans can move into the 90- to 180-day range. and foreclosure activity generally starts only later. when a borrower is at least 120 days delinquent.. Misryoum notes that this ladder matters because today’s early-stage delinquencies often foreshadow where foreclosure risk could concentrate tomorrow.

Insight: Foreclosure is usually the end of a longer process. Tracking early delinquencies gives markets and policymakers a faster signal than waiting for defaults to become visible.

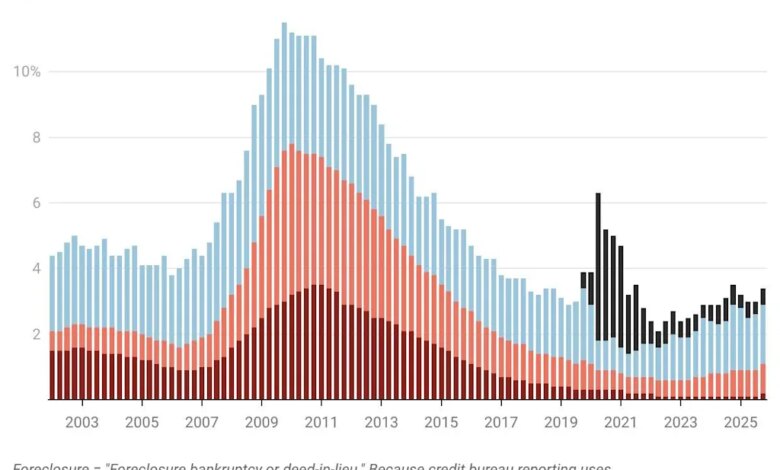

Right now, the overall pipeline of mortgage distress is still small compared with past crises, but it is growing.. Misryoum reports that early-stage delinquencies have been ticking upward since 2022, with more serious delinquencies following the same direction.. The shift fits a broader story of housing markets slowly moving out of the unusual conditions that prevailed during the pandemic years.

That context is important.. During COVID-19, a nationwide foreclosure moratorium and extended forbearance protections helped delay foreclosure outcomes.. Meanwhile. a surge in homebuyer demand pushed prices higher and boosted homeowner equity. contributing to historically low foreclosure and serious delinquency rates around 2021.. As these protections have gradually expired. the underlying stress that was deferred rather than eliminated has started to surface again in delinquency data.

Insight: As support programs unwind, the question for homeowners and lenders changes from “Will defaults happen?” to “How quickly will delayed stress show up in different regions?”

Misryoum also frames the current moment with perspective against the Great Financial Crisis era.. Total housing distress levels today are elevated compared with the pandemic low. but they remain far below the peak levels seen in the late 2000s and early 2010s.. In other words. while the direction is clearly less forgiving than during the boom. it does not point to a system-wide breakdown on the scale of 2008–2011.

Still, the risk is not evenly distributed.. Misryoum highlights particular concern involving government mortgage programs, including FHA, USDA, and VA.. FHA mortgages. often used by first-time and lower-income buyers. have shown a notable increase in delinquencies over the past two years.. Misryoum also notes that government-insured mortgages make up a meaningful share of outstanding debt nationwide. which means shifts in those pools can have outsized impacts in specific communities.

Insight: Even when national totals look contained, regional and program-level stress can move differently, so “average” numbers can mask the hardest-hit neighborhoods.

Geography adds another layer.. Misryoum reports that the highest concentration of housing distress is not primarily in the biggest pandemic boom markets that are working through post-boom corrections.. Instead, Louisiana and Mississippi stand out as key areas of concern, influenced by broader insurance shocks and consumer credit stress.. The article also flags that some areas in these states have seen pricing weakness even without the same kind of prior run-up seen in other Sun Belt markets.

Meanwhile, most other markets remain at distress levels well below those seen at the start of the last major downturn. For now, Louisiana is the standout exception, suggesting that local economic pressures can dominate even when national conditions are improving.